SKOCH aims to steer FinTechs away from hype and help them see and address a real market through a fine balancing act between both supply side and demand side issues.

Register Now Read More Download BrochureSKOCH FinTech Awardees

Financial Inclusion Task Force (FITF)

Task Force Member

U K Sinha

Former Chairman, SEBI

U K Sinha - Former Chairman, SEBI

Upendra Kumar Sinha is the former chairman of SEBI. He was the Chairman and Managing Director (CMD) of the Unit Trust of India Asset Management Company (UTIAMC), commonly referred to as UTI Mutual Fund. He has also chaired the RBI expert committee on Micro, Small and Medium Enterprises/He received SKOCH Challenger Golden Jubilee Award for his contribution to market reforms during his tenure as Chairman at SEBI.

Task Force Member

S S Mundra

Chairman, BSE

S S Mundra - Chairman, BSE

Shri S.S. Mundra retired as Deputy Governor of Reserve Bank of India on 30th July 2017 after completing a stint of three years. Prior to that, the last position held by him was as Chairman and Managing Director of Bank of Baroda from where he superannuated in July 2014. In a banking career spanning over four decades, Shri Mundra held several important positions including that of Executive Director of Union Bank of India, Chief Executive of Bank of Baroda (European Operations) amongst others. He also served as RBI's nominee on the Financial Stability Board (G20 Forum) and its various committees. Shri Mundra was also the Vice-chair of OECD's International Network on Financial Education (INFE).

Prior to joining RBI, Shri Mundra also served on Boards of several multi-dimensional companies like the Clearing Corporation of India Ltd (CCIL), Central Depository Services (India) Ltd. (CDSL), BOB Asset Management Company, India Infrastructure Finance Corporation (UK) Ltd. (IIFCL), IndiaFirst Life Insurance Company Ltd., Star Union Dai-Ichi Life Insurance Company Ltd., National Payments Corporation of India Ltd., etc. The experience gained in guiding these entities has bestowed him with wide leadership skills and keen insights in best practices in Corporate Governance.

Shri Mundra has been a regular presence as a Speaker on various Forums. He has delivered more than 60 speeches/presentations on diverse issues viz. banking, financial inclusion & literacy, MSME financing, audit, Fraud Risk Management, Cyber security, Consumer Protection, Human Resource Management etc. at both domestic and international forums. Many of these speeches have been published on the websites of Reserve Bank of India and that of the Bank for International Settlements.

Task Force Member

Amarjeet Sinha

Former Union Rural Development Secretary

Amarjeet Sinha - Former Union Rural Development Secretary

Shri Amarjeet Sinha is a Graduate in History. He is a 1983 batch IAS Officer of the Bihar Cadre holding the post of Secretary, Ministry of Rural Development, Government of India.

He has over 30 years of experience in government, largely in the social sector. He has had the unique distinction of having played a major role in designing Sarva Shiksha Abhiyan (India's main program for universal elementary education) and the National Rural Health Mission. He has also been training Indian Administrative Service Officer Trainees at the Lal Bahadur Shastri National Academy of Administration, Mussoorie on the social sector over the last one and a half-decade.

Amarjeet has published seven books and a large number of articles in publications such as The Lancet, Economic and Political Weekly, Economic Times, The Hindu, The Business Standard, The Hindustan Times, etc. His latest book, “An India for Everyone - A Path to Inclusive Development”, was released by Nobel Laureate Amartya Sen on February 2013.

Task Force Member

Sameer Kochhar

Chairman, SKOCH Group

Sameer Kochhar - Chairman, SKOCH Group

Reforms historian and author of best-seller ModiNomics, Sameer Kochhar is Chairman, SKOCH Group. He is a passionate advocate of social, digital and financial inclusion and is a foremost expert on governance and inclusive growth. His work has been acclaimed globally and endorsed by Mr Narendra Modi, Mr M Venkaiah Naidu, Dr Manmohan Singh, Mr Arun Jaitley, Mr P Chidambaram, Mr Yashwant Sinha, Dr C Rangarajan and Dr Montek Singh Ahluwalia and so on. In his thinking and writings and activities, his profound admiration for India's economic reforms and in extension, those outstanding personalities who strive to make these reforms more meaningful and broad-based comes out clear and unambiguous.

Task Force Member

Deepali Pant Joshi

Former Executive Director, RBI

Deepali Pant Joshi - Former Executive Director, RBI

Dr Deepali Pant Joshi is a career banker and has served the Reserve Bank of India for more than three and a half decades. She headed various departments in RBI including Departments of Rural Planning and Credit and Financial Inclusion Department and Customer Services & Financial Education Department. During her long career with the Regulator, she also held some key positions like Banking Ombudsman for the State of Andhra Pradesh, Regional Director at RBI, Jaipur, heading RBI Banking operations in Rajasthan, Principal of Bankers Training College, Mumbai, etc.

Dr Deepali Pant Joshi also held various Board positions, to name a few: nominee Director on the Board of Institute of Banking Personnel and Selection (IBPS), Andhra Bank, nominee Director on the Board of NABARD for the supervision of Co-operative Banks & RRBs, nominee Director on Bhartiya Note Mudran Press Ltd., etc. Presently she is an Independent Director on the Board of Multi Commodities Exchange of India Limited and a Governing Council Member of Sa-Dhan, a Self-Regulatory Organization for micro-Finance Institutions in India.

Dr Deepali Pant Joshi has been appointed on the Board of NABFINS with effect from January 19, 2021.

She holds a D Phil from the University of Allahabad. She also has Law and Management degrees. She is a fellow of the Harvard University Asia Center.

Task Force Member

Siraj Hussain

Former Union Agriculture Secretary

Siraj Hussain - Former Union Agriculture Secretary

Siraj Hussain is currently a Senior Visiting Fellow at Indian Council for Research on International Economic Relations (ICRIER). He joined the Indian Administrative Service in 1979 and has served the Government of Uttar Pradesh in various capacities including District Magistrate, Managing Director, State Industrial Development Corporation, Registrar of Cooperative Societies, and Secretary to Chief Minister. In the Government of India, he has worked as Joint Secretary, Department of Food and Public Distribution and Chairman and Managing Director of Food Corporation of India (FCI). He was posted as Union Secretary in the Ministries of Food Processing Industries and Agriculture. Several schemes of the first Modi government were formulated under his supervision as Secretary, Agriculture. He has authored several research papers on agriculture and the rural economy and his columns have been published in several newspapers and online portals.

Task Force Member

Reema Nanavaty

Director, SEWA

Reema Nanavaty - Director, SEWA

Reema Nanavaty leads Self Employed Women's Association's (SEWA) economic and rural development activities reaching out to seventeen million women and their families across India.

Since 1989 she has pioneered revival, restoration and innovation of rural livelihoods from district to global level. Reema is being recognized across India and in the neighbouring countries as a champion of making livelihoods of the poor women reach markets they deserve. May they be women artisans, salt pan workers, farmers, or labourers, she has made efforts over two decades to mainstream amazing diversity of skills and knowledge of India's citizens into the national mainstream. Her effort has created a more dynamic local economy and fairer and equal society for thousands of SEWA sisters, citizens of India.

Born on May 22, 1964 in Ahmedabad, Reema graduated in science from Gujarat University and was selected to IAS services of Government of India.

Task Force Member

Chandra Shekhar Ghosh

MD & CEO, Bandhan Bank

Chandra Shekhar Ghosh - MD & CEO, Bandhan Bank

Mr. Ghosh has been one of foremost proponents of microfinance in India. He has more than 30 years of experience in the microfinance and development spaces. He founded Bandhan in 2001 as a not-for-profit enterprise that stood for financial inclusion and women empowerment through sustainable livelihood creation. He was on the forefront of its transformation into an NBFC-MFI and finally a universal bank in August 2015.

Mr. Ghosh is the former President of Bengal Chamber of Commerce & Industry (BCC&I) and the former Chairman of CII, Eastern Region. He is also a member of Managing Committee of Indian Banks' Association (IBA) and a member of Corporate Governance Council, CII. He co-chairs the Financial Inclusion Committee of Federation of Indian Chambers of Commerce and Industry (FICCI). Further, he is a member of the Committee on Micro, Small and Medium Enterprises (MSME) sector, Government of West Bengal, along with being a member of College Advisory Committee (CAC) in CAB, Pune. He has also been a distinguished invitee on the Council of Management, AIMA. Mr. Ghosh was elected as 'Senior Ashoka Fellow' in 2007 by Ashoka Foundation (social entrepreneurship award).

He holds an MSc in Statistics and also attended the HBS-ACCION programme on Strategic Leadership at Harvard Business School in April 2006. He has completed a Certification Programme in IT & Cyber Security conducted by Institute for Development and Research in Banking Technology (IDRBT), established by the Reserve Bank of India.

Task Force Member

Ajit Ranade

VC, Gokhale Institute of Politics & Economics

Ajit Ranade - VC, Gokhale Institute of Politics & Economics

He earlier served as an Executive Officer of Financial Technologies India Ltd. and Chief Economist at ABN AMRO Bank. His professional career has spanned academic and corporate assignments, including teaching in India and U.S. Dr. Ranade serves as a Director on the Board of Hindalco Almex Aerospace Limited, a joint venture company of Hindalco and Almex Inc. of USA. He has served on various committees of the Reserve Bank of India, most recently in the committee for Fuller Capital Account Convertibility.

Task Force Member

Deepak B Phatak

IIT-B, Mumbai

Deepak B Phatak - IIT-B, Mumbai

Dr Deepak B Phatak is Chair Professor at Indian Institute of Technology-Bombay, India. He graduated in Electrical Engineering from Indore and then completed his MTech and PhD in Computer Science. He is with IIT Bombay since 1971.

He served in the Department of Computer Science and Engineering till January 2000 and was the Department head from 1991 to 1994. He also served as the first Dean of Resource Development for IIT Bombay from 1995 to 1998. He was invited to head the Kanwal Rekhi School of Information Technology set up in October 1998 at the Institute.

He has been an eminent consultant and advisor to many organisations on various issues related to Information Technology.

In the financial sector, he has involved in a major effort by Industrial Development Bank of India, and has been an I.T. advisor to the State Bank of India for several years. He has also been a consultant to several other financial and industrial organisations like Reserve Bank of India, Unit Trust of India, Industrial Credit & Investment Corporation of India, Life Insurance Corporation of India, New India Assurance, Rashtriya Chemicals and Fertilisers, L&T, Times of India, etc.

He works on several committees advising Government departments on issues related to computerisation. Dr Phatak is on the boards of IDBI Bank, ISIL, UTIISL, NIBM, IDRBT, Bank of Baroda, and NIA. He has recently published an edited book entitled Infrastructure and Governance.

Task Force Member

S Mahendra Dev

Chairperson, Institute for Development Studies

S Mahendra Dev - Chairperson, Institute for Development Studies

S. Mahendra Dev has been the Director and Vice Chancellor of the Indira Gandhi Institute of Development Research (IGIDR) in Mumbai, India, since 2010. Prior to this, he was Chairman of the Commission for Agricultural Costs and Prices for the Ministry of Agriculture of the Government of India, Director of the Centre for Economic and Social Studies in Hyderabad, and Acting Chairman of the National Statistical Commission of the Government of India. He is a recipient of the Malcolm Adiseshiah Award for outstanding work on development studies and has approximately 120 research publications in international and national journals in the areas of agricultural development, poverty, public policy, inequality, food security, nutrition, employment guarantee schemes, social security and farm and nonfarm employment. He has written or edited 20 books, including Inclusive Growth in India. He is a member of the Board of Trustees of the International Food Policy Research Institute and was nominated to serve as Vice Chair of the Board beginning in 2018. He has been a consultant and adviser to many international organizations, including the United Nations Development Programme, the World Bank, the International Labour Organization, the Food and Agriculture Organization of the United Nations, United Nations Economic and Social Commission for Asia and the Pacific, UNICEF, UNESCO, the UK Department for International Development, and the Organization for Economic Cooperation and Development. He received his PhD from the Delhi School of Economics and completed his postdoctoral research at Yale University.

Task Force Member

Renana Jhabvala

Chairperson, SEWA Grih Rin Ltd

Renana Jhabvala - Chairperson, SEWA Grih Rin Ltd

Renana Jhabvala is an Indian social worker, best known for her long association with SEWA (Self Employed Women's Association). She has been active for decades in organizing women into trade unions in India. She is currently the Chairperson of SEWA Bharat and the national coordinator of SEWA.

A Padma Shri awardee, she has represented SEWA at the International Labour Organization (ILO) and other international forums. She was also instrumental in forming HomeNet South Asia and has been one of the founders of WIEGO (Women in Informal Employment: Globalizing and Organizing). She has been active in many Government committees and task forces in India which have formulated a wide range of policies, National Policy for Urban Street Vendors in India, being a key one.

Renana Jhabvala has a BA in Mathematics from Hindu College, Delhi University and an MA in Economics from Yale University, USA.

Abhiman Das

RBI Chair Professor in Finance & Economics, IIM - Ahmedabad

Prof Abihman Das is a Professor of Economics at the Indian Institute of Management Ahmedabad. He has been working in various capacities in the Department of Statistics and Information Management (Research Department) of the Reserve Bank of India (RBI) for over two decades. Before Joining the IIMA, he was holding the post of Director (General Manager) at the RBI.

He was member of the Editorial Committee of Reserve Bank of India Working Paper Series, 2014-15 and Reserve Bank of India Occasional Papers, 2010-12.

Abhiman Das was post-Doctoral Research Fellow at Massachusetts Institute of Technology (MIT), Department of Economics, Cambridge, US and holds a Ph.D. (Population Studies)degree from International Institute for Population Sciences, Bombay.

Task Force Member

Ajay Thakur

Head, BSE SME

Ajay Thakur - Head, BSE SME

He is credited for launching the first ever SME Platform and Startup Platform in India on 13th March, 2012 and 22 December, 2018 respectively. BSE today is the largest SME Platform in India with 325 companies listed and 55 companies are in pipeline. These 325 companies listed represent 17 sectors which has raised an amount of Rs.3340.36 crores with market capitalization of Rs. 18,528.71 crores. BSE has got 5 Startups listed in its Startup Platform which has raised 22.24 crores with market capitalization Rs 82.71 crores. There are another 5 Startups which are in pipeline to get listed. The success of these platforms has been recognized and appreciated by national and international organizations.

In one of the annual issues of 2013, Asian Development Bank (ADB) has appreciated the effort of BSE SME for promoting SME listing in India. IOSCO also in its research report of July 2015 mentioned that BSE SME platform is the most cost effective platform for SME listing in the World. BSE SME has received SKOCH achiever award from the hands of then, Minister of State for finance Shri Jayant Sinha in the year 2015. BSE has been also awarded as the best SME exchange in India by Shri Kalraj Mishra, then Minister for MSME in 2016 and from SP Jain Institute of Management and Research as CHANGE AGENT in the year 2018. Mr. Ajay thakur is also on various committees viz, India SME Forum and CII MSME Committee.

Task Force Member

Jayshree Vyas

MD, Mahila Sewa Sahakari Bank

Jayshree Vyas - MD, Mahila Sewa Sahakari Bank

Ms Jayshree Vyas, a chartered accountant by profession, is an independent director of Village Financial Services.

Besides being the Managing Director of Shri Mahila Sewa Sahakari Bank Ltd and Promoter Director in Sewa Grih Rin Ltd, she is also a managing trustee in Indian School of Microfinance for Women, Ahmedabad, a trustee and Chair of Mahila Housing Trust, a director in Equitas Holding Ltd, Friends of Women's World Banking, Ananya Finance for Inclusive Growth Pvt Ltd, Sewa Trade Facilitation Centre, and VimoSEWA, among others.

She has helped introduce an integrated micro-insurance scheme for women working in the informal sector, the first such in India. She has also devised housing finance schemes for poor women and savings groups of poor women in Gujarat. In 2006, under her leadership, Sewa Bank introduced a Micro Pension Scheme.

Anil Bhardwaj - Secretary General, FISME

Anil Bhardwaj is Secretary General of Federation of Indian Micro Small & Medium Enterprises (FISME). He has worked extensively in the fields of international trade and SME development. He has advised or led several SME development projects supported by multilateral and bilateral donor agencies in India. His recent engagements include: Member, Damodaran Committee for Reforming the Regulatory Environment for Doing Business in India (Ministry of Corporate Affairs); Member, Drafting Committee for 'National Voluntary Guidelines on Social, Environmental and Economic responsibilities of Business' since notified by Ministry Corporate Affairs (Govt. of India); Member, Advisory Group of IICA-GIZ CSR initiatives; Member, Project Advisory Committee 'National Competition Policy and Economic Growth in India'

Alok Misra - CEO & Director, MFIN

Dr. Alok Misra has 30 years of professional experience in international development, rural finance, microfinance, inclusive finance and research at both policy and implementation level. He started his career with India's apex rural development bank (NABARD) in 1992 wherein his work spanned various areas of development finance. He was also a part of the multi-institutional task force (2003-2004) responsible for setting up India's first online demutualized commodities exchange (NCDEX).

In 2008, he shifted to a global microfinance rating, policy analysis and technical advisory agency. Before coming to MFIN as CEO & Director, Dr. Misra was Professor and Chairperson, School of Public Policy & Governance at Management Development Institute (MDI), Gurgaon. He has served as a Board member of MFIN, Vaya Finserv and member of NABARD's strategic group on microfinance. He is a member of Inclusive Finance India Group of Advisors, member of Digital finance working group constituted by ITU, Geneva. He has worked across 24 countries in Asia, Africa, Europe, and Pacific. He has written numerous articles and reports and authored "Inclusive Finance India report" for two years.

Dr. Alok Misra holds a PhD in Development Studies from Victoria University of Wellington, Master in Development Management (Gold Medalist) from Asian Institute of Management, Manila. He was awarded ADB-Government of Japan scholarship for MDM programme and NZAID scholarship for his PhD. He has been trained at Harvard Business School in "Strategic leadership for Microfinance" and was a Fellow, Fletcher Leadership Program for Financial Inclusion at Tufts University.

Jiji Mammen - ED & CEO, San-Dhan

Jiji Mammen, ED & CEO, Sa-Dhan superannuated from NABARD after a long career of nearly 37 years on 31 May 2022. After the superannuation he joined Sa-Dhan as its CEO. During his tenure in NABARD he served in various capacities and responsibilities. This included working as District Development Manager of Kottayam district, Faculty Member of BIRD, Mangalore campus, Officer in Charge of Manipur State, CGM and OIC of Rajasthan, Andhra Pradesh and Telengana Regional Offices. He was the first CEO & MD of MUDRA Ltd. He also served as Managing Director of NABFINS Ltd, a subsidiary MFI of NABARD.

Jiji Mammen is a Post graduate in Agriculture Sciences from IARI, New Delhi. He also did LLB from Kerala University and a Associate member of IIBF ( CAIIB). His areas of expertise include micro credit, micro enterprises, agriculture project lending.

The objective of financial inclusion is to extend the scope of activities of the organised financial system to include within its ambit people with low incomes. Through graduated credit, the attempt must be to lift the poor from one level to another so that they come out of poverty.

The Modi Government has laid the necessary infrastructure and made considerable progress to make this happen. It has achieved the objective of universal banking. DBT has been a great success. Over six crore PMJDY account holders have received DBT from various schemes. The beginning was made on 15th August 2014, when the Hon'ble Prime Minister announced PMJDY to fulfill the objective of universal financial inclusion taking banking to the last mile.

SKOCH Model of Inclusive Growth featured for the first time in the book, Financial Inclusion (2008) and shortly followed in the next book, Speeding Financial Inclusion (2009). These books had a pronounced policy impact. Most recommendations were accepted and implemented. ModiNomics (2014) again argued for inclusive economics and inclusive governance as per Modi Ji's Gujarat model.

The third book Defeating Poverty: Jan Dhan and Beyond (September 2014) contributed to the current spate of policy interventions like DBT, MUDRA, overdraft in Jan Dhan accounts and Payments. The roadmap for public digital infrastructure for financial inclusion was laid out in Modi's Odyssey: Digital India, Developed India (2016).

We have formed a Financial Inclusion Task Force (FITF) under the aegis of the SKOCH Development Foundation and the CEO's Association for Inclusive Growth (CAII) to return recommendations on digital lending and markets - bridging credit & literacy gaps.

Financial InclusionEditors: Sameer Kochhar

R. Chandrashekhar

K.C. Chakrabarty

B. Phatak

(2008)

Speeding Financial InclusionPredace: C. Rangarajan

Introduction: K.C. Chakrabarty

(2009)

ModiNomicsSameer Kochhar

(2014)

Defeating Poverty

Jhan Dhan and BeyondSameer Kochhar

Preface: Yashwant Sinha

Foreword: C. Rangarajan

(2014)

Modi's Odyssey

Digital India, Developed IndiaSameer Kochhar

(2016)

SKOCH FITF Findings

Modi Government Makes Great Stride in Financial Deepening by Sameer Kochhar

I have been analysing and writing on the issues related to financial inclusion for more than two decades. The National Sample Survey of 2005 drew the media and the policymakers’ attention to the issue of financial exclusion. As per the survey report, just around 27 per cent of farm households had access to formal sources of finance.

The objective of Financial Inclusion is poverty alleviation. Data in India needs to be more comprehensive, accessible and reliable. Every report starts a raging debate on the number of poor, the number of jobs, the state of inequality, etc. Most of my work over the past decades relates to out-of-thebox macro research and co-relating the same with actual primary field research and case studies. I find not-so-obvious evidence that shows what is working and what is not.

In February 2011, the Swabhimaan scheme was launched to ensure basic banking services to unbanked villages with a population of 2,000 and above by March 2012. I have noted the reasons for the sub-optimal performance of the Swabhimaan scheme in my book ‘Defeating Poverty: Jan Dhan and Beyond’.

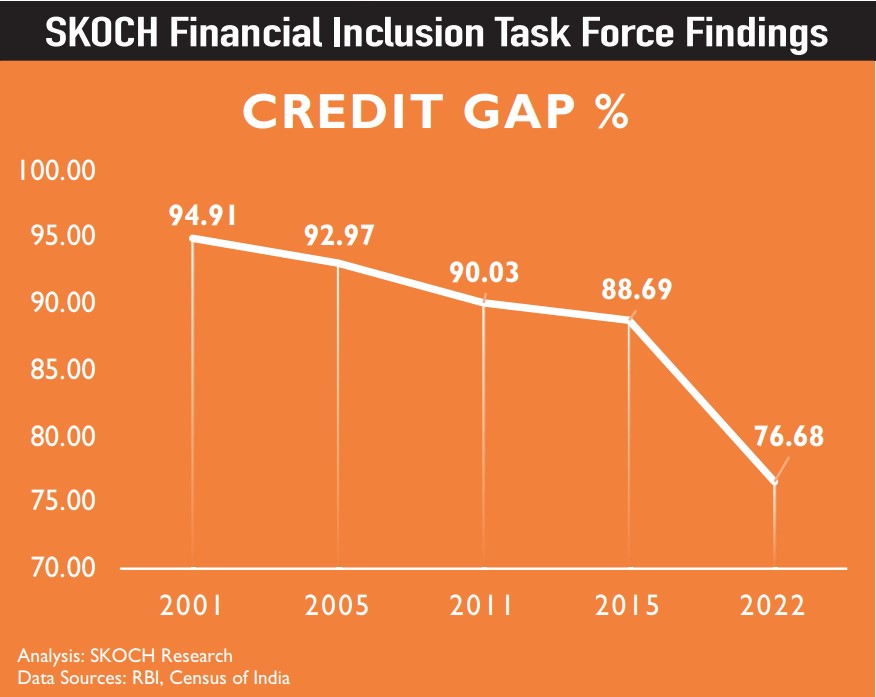

Credit Gap Falls 12.01% - Modi Government Speeds Financial Inclusion

Credit gaps in India declined by 12.01 percentage points in seven years between 2015 and 2022 as against a mere 6.22 percentage points drop in the previous 14 years between 2001 and 2015, showing impressive outcome of the Financial Inclusion initiatives taken by Prime Minister Narendra Modi government, according to a report released by SKOCH Financial Inclusion Task Force ahead of the Union Budget 2023-24.

In 2001, credit gaps in India stood at 94.91 per cent. This declined marginally to 92.97 per cent in 2005 and further to 90.03 per cent in 2011 and 88.69 per cent in 2015. Though there was a consistent decline in credit gap between 2001 and 2015 but the progress was marginal.

Considerable progress was witnessed between 2015 and 2022. During this 7 year period, the credit gap fell from 88.69 per cent in 2015 to 76.68 per cent in 2022, registering a decline of 12.01 percentage points.

Credit gap refers to the proportion of people having no access to formal credit. SKOCH Financial Inclusion Task Force research report on credit gaps uses the same methodology of calculation as used by the Rangarajan Committee in its report released in 2008. A Committee on Financial Inclusion headed by former RBI Governor C Rangarajan analysed credit gaps for the year 2005.

Latest Features

Terms of Reference

Approach

Call for Submissions

Submissions are invited from stakeholders in Financial Inclusion journey of India:

• Met and Unmet Needs

• Opportunities and Challenges

• Solutions for enhancing credit penetration

• Solutions for enhancing Financial Literacy

• Innovative ways of raising finance, sureties and collateral

• Existing research, initiatives and inputs

• Selected submissions will be acknowledged and invited for presentation

Last Date: 15th May 2025

SKOCH FinTech Forum 2023

SKOCH FinTech Forum aims to steer FinTechs away from hype and help them see and address a real market through a fine balancing act between both supply side as well as demand side issues.

We intend to bring technology and service providers, consumers of credit, regulators, and policymakers on the same page to chart out an actionable agenda.

India has huge unmet needs in Financial Products and Services. This gap was unaddressed due to a lack of enabling technology. Now that the technology is available, a better understanding of the credit gaps and literacy issues would be key success factors for FinTechs to be able to address the real market.

Most FinTech strategies are based on regulatory arbitrage, technology-based policy influencing, and traditional money burn and market capture models. While there seem to be advisors aplenty for these, few address issues or have competence in multi-disciplinary areas like the cost of money, generating resources from markets, and newer underwriting and collateral models.

SKOCH FinTech Forum once again leverages our years of ground research, our proven policy interventions, and our passion for Financial Inclusion since inception to steer India towards the next step of SKOCH Financial Inclusion Model, ie availability of abundant credit and financial literacy to effectively access and deploy it. SKOCH FinTech Forum will see the release of the report of the Financial Inclusion Task Force.

It would be the first such report with wide-ranging ramifications.

Download BrochureSKOCH FinTech Award

Receiving a SKOCH Award is the best way to garner the attention of all relevant stakeholders.

It brings instant visibility and fame for the product amongst its customers, regulators, policymakers and other important stakeholders.

Given the rigour of the process, it is considered India's highest independent honour and is received and celebrated by ministers, Chief Ministers, Bureaucrats and Industry leaders alike.

Nominations are invited for SKOCH FinTech Award for exceptional / innovative products, achievements and corporate contributions to Digital Financial Inclusion. Evaluations would be by a Jury to identify products, services and organisations to take note of, learn from and replicate.

The nomination(s) can be submitted online on the apply page. For any assistance you may reach our award secretariat at fintech@skoch.in.

How to apply for|participate in|win SKOCH FinTech Award?

Early Bird: 15th May 2025 | Conference Delegate Fee (for 4 Individuals from one organisation): Rs 35,000 + GST@18%

Last Date: 30th May 2025 | Conference Delegate Fee (for 4 Individuals from one organisation): Rs 40,000 + GST@18%

Go to Apply PageStep 1

Submit NominationStep 2

Delegate RegistrationStep 3

Are you a FinTech serious about Business?

Participate

Register as a Delegate in SKOCH FinTech Forum:

delegate.fintech.skoch.in

SKOCH Awardees*

* All brand logos above are registered trademarks or trademarks of their respective companies/organisations.

* These are some of the past awardees. Full list can be viewed at Past SKOCH Awards page.

Forum Calendar

Upcoming Conferences

About SKOCH Group

SKOCH Group is India’s leading think tank dealing with socio-economic issues with a focus on inclusive growth since 1997. SKOCH Group is able to bring an Indian felt-needs context to strategies and engages with fortune-500 companies, state owned enterprises, government to SMEs and community-based organisations with equal ease.

Phone: 0124-4777444Email: info@skoch.in

Our Mission

The repertoire of services include field interventions, consultancy, research reports, impact assesments, policy briefs, books, journals, workshops and conferences. SKOCH Group has instituted India's highest independent civilian honours in the field of governance, finance, technology, economics and social sector. The group companies include a consulting wing, SKOCH Consultancy Services Private Limited; a media wing, SKOCH Media; and a charitable foundation, SKOCH Development Foundation.